By DAVID STREITFELD

Published: May 31, 2011

Housing prices fell in March to their lowest point since the downturn began, erasing the last little bit of recovery from the depths achieved two years ago, according to data released Tuesday.

Multimedia

Readers' Comments

Share your thoughts.

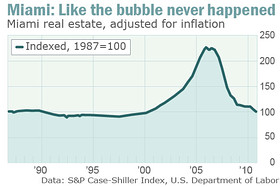

The Standard & Poor’s Case-Shiller Home Price Index for 20 large cities fell 0.8 percent from February, the eighth drop in a row. Prices are now down 33.1 percent from July 2006 peak.

“Home prices continue on their downward spiral with no relief in sight,” said David M. Blitzer, chairman of the S.& P. index committee.

Housing is in persistent trouble, industry analysts say, not only because so many people are blocked from the market — being unemployed, in foreclosure or trapped in homes that are worth less than the mortgage — but because even those who are solvent are opting out.

“The emotional scars left by the collapse are changing the American psyche,” said Pete Flint, chief executive of the housing Web site Trulia. “There was a time when owning a home was a symbol you had made it. Now it’s O.K. not to own.”

Trulia, a real estate search engine for buyers and renters that is based here, is a hive of renters, including Mr. Flint. “I’m in no rush at all to buy,” he said. He expects homeownership to decline further to about 63 percent, a level the country first achieved in the mid-1960s.

The desire to own your own home, long a bedrock of the American Dream, is fast becoming a casualty of the worst housing downturn since the Great Depression.

Even as the economy began to fitfully recover in the last year, the percentage of homeowners dropped sharply, to 66.4 percent, from a peak of 69.2 percent in 2004. The ownership rate is now back to the level of 1998, and some housing experts say it could decline to the level of the 1980s or even earlier.

Tim Hebb, a Los Angeles systems engineer, expertly called the real estate bubble. He sold his bungalow in August 2006, then leased it back for a year. Since then, the 61-year-old single father has rented a succession of apartments.

“I have flirted with buying again many times over the past few years,” said Mr. Hebb. “Let’s face it, people are not rational creatures.”

But he always resists, figuring housing is still overpriced and even when it stops declining it will stumble along the bottom for years and years. He says there is plenty of time to get back in if he should ever want to.

The market signaled further trouble on Friday when the April index of pending deals was released by the National Association of Realtors. Analysts had predicted the index, which anticipates sales that will be completed in the next two months, would be down 1 percent from March. Instead, it plunged 11.6 percent.

Many of those in the business of building and selling houses believe the current disaffection with real estate will pass. After every giddy boom comes the hangover, they acknowledge, but that deep-rooted desire for a castle of one’s own quickly reasserts itself.

There’s no question that people are reluctant to own, said Douglas C. Yearley Jr., chief executive of Toll Brothers, the builder of high-end homes. “They’re renting and they’re happy renting because they’re scared.”

Yet those fears will fade, he predicted.

“Most people still want the big house with the big lot in the desirable school district in the suburbs. No one ever renovated the kitchen or redid a room for the kids in a rental,” Mr. Yearley said. “I think — I hope — we’ll be O.K.”

The market’s persistent weakness, however, runs the risk of feeding on itself. Buyers are staying away despite the lowest interest rates and the highest affordability levels in many years, which in turn prompts others to hesitate.

Trulia and another real estate site, RealtyTrac, commissioned Harris Interactive to take a poll last November about when people thought the market would recover. A third of the respondents chose 2014 or later. But in a new poll, released this month, the percentage giving that answer rose to 54 percent.

The sharp decline in prices since 2006 has meant a lost decade for many owners. But what may prove even more discouraging to potential buyers is academic research showing that the financial rewards of ownership were uncertain even before the crash.

In a recent paper, a senior economist at the Federal Reserve Bank of Kansas City found that the notion that homeownership builds more wealth than investing was true only about half the time.

“For many households in many years, renting and investing the saved cash flow has built more wealth than homeownership,” the economist, Jordan Rappaport, concluded.

Economics affects potential owners in other ways. A house is a long-term commitment that many are loath to make in uncertain times like these.

“What I’m hearing from people is that they don’t want to be tied to a particular geography, which inclines them to renting,” said Mr. Flint of Trulia.

San Francisco is one of the country’s most expensive cities, so renting has a natural appeal here. But the Associated Estates Realty Corporation, which owns 13,000 apartments in Georgia, Indiana, Michigan and other Midwest and Southeast states, also is seeing more people deciding to rent.

“We have more of what we call ‘renters by choice’ than I’ve seen in the 40 years I’ve been in the apartment business,” said Jeffrey I. Friedman, chief executive of Associated Estates.

For decades, the company has asked former tenants why they were moving out. During the housing boom, as many as a quarter of those moving on said they were buying a house. In 2009, the percentage of new owners fell in the first quarter to 13.7 percent, the lowest ever.

Last year, as the economy improved, the number rebounded. This year, it fell back again, to 14 percent.

Builders clearly believe that the future includes many more renters. So far this year, construction of multiunit buildings is up 21 percent compared with 2010, while single family-homes are down 22 percent. Sales of new single-family homes are lower than at any time since the data was first kept in 1963.

Susan Lindsey, a San Diego software programmer, was once eagerly waiting for the housing market to crash. She said she would have no guilt about swooping in on some foreclosed owner who had bought a place he could not afford.

With prices now down by a third, however, she is content to stay in her $2,500-a-month rented house. She prefers to invest in gold, which she has been buying since 2003.

“I could afford a median-priced house, no problem,” said Ms. Lindsey, 48, as she headed off for a holiday weekend in Las Vegas. “But I would be paying more to live in a place I like less.”